Adult Use Cannabis Tax

Adult Use Cannabis Excise Taxes are imposed on cannabis and cannabis products sold by a licensed adult use cannabis retailer.

Retailers who sell cannabis and cannabis products to consumers at retail.

Yes.

Yes.

No. However, the compassion centers and hybrid cannabis retailers must continue to file and pay the monthly Compassion Center Surcharge Returns and monthly sales tax returns.

The filing and payment for State and Local Cannabis Excise Taxes are due on or before the 20th day of each month for the previous calendar month when the sale was made.

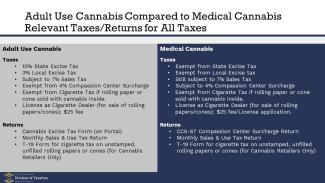

The State Cannabis Excise Tax is computed on the selling price at the rate of 10%. The Local Cannabis Excise Tax is computed on the selling price at the rate of 3%.

All adult use cannabis retail sales are subject to the Cannabis Excise Taxes and Sales and Use Taxes.

Exemptions for State and Local Cannabis Excise Taxes only apply to the following:

-

Medical sales

-

Sales to "Cannabis establishments" as defined in R.I. Gen. Laws § 21-28.11-3

For Sales and Use Tax exemption information, please refer to the Sales & Use tax page.

Each of the interest and penalty amounts, as provided for in statute, are separately stated below:

-

Interest applies at the annual rate pursuant to R.I. Gen. Laws § 44-1-7 and shall be imposed for a failure to pay the State Cannabis Excise Tax when it is due.

-

Failure to file penalty: 10% of the amount of the tax due.

-

Failure to pay penalty: 10% of the amount of the tax due.

-

Negligence penalty: 5% of the deficiency that results from negligence or intentional disregard of the law.

-

Fraud penalty: 50% of the deficiency that results from fraud. This penalty will be in lieu of any other penalties imposed above.

-

Failure to collect and pay: 100% of the tax evaded, not collected, or not accounted for and paid.

-

Additional penalties may apply under R.I. Gen. Laws §§ 44-18, and 44-70, and other relevant provisions.

Yes. Some of the other taxes/fees are listed below:

-

Sales Tax: filed monthly and is imposed on the total sales price, including any fees associated with the sale.

-

Litter Control Permit Fee: filed annually and is calculated using the entity’s gross receipts from the prior year.

Other taxes/fees may apply depending on other aspects of the business and the specific circumstances of each transaction.

A Cigarette Tax is imposed on each sheet of cigarette rolling paper, including but not limited to, paper made into a hollow cylinder or cones, made with paper or any other material, with or without a filter suitable for use in making cigarettes at the tax rate determined by R.I. Gen. Laws §44-20-1, et seq.

If any of the above products are sold with cannabis inside, they are not subject to the Cigarette Tax. However, if the above products are sold individually, they would still be subject to the Cigarette Tax. There are two ways this tax requirement can be fulfilled:

-

Cigarette rolling papers and cones can be purchased from a licensed cigarette distributor with the tax prepaid; or

- The cannabis retailer must file a Form T-19 to pay the tax. This form can be obtained from our Excise and Estate Tax Section through email at Tax.Excise@tax.ri.gov or by calling 401-574-8955.

Some of the other licenses/permits that may be required are listed below:

-

Sales Tax Permit: Valid from July 1st through June 30th and is renewable annually (must be requested by February 1). There is no cost associated with this permit.

-

Litter Control Participation Permit: Valid from January 1st through December 31st and is renewable annually (must be requested by August 1). The cost of the permit depends on the gross receipts of the entity.

-

Dealer's License: Valid from July 1st through June 30th and is renewable annually (must be requested by February 1). The cost of this permit is $25.00 annually.

Yes. The two statutes are reciprocal and impose the same taxes only once.

No, the State and Local Cannabis Excise Taxes are not subject to Sales and Use Tax.

All medical sales of cannabis must be purchased by an “Authorized purchaser”, or “Cardholder” as defined in R.I. Gen. Laws § 21-28.6-3. The cannabis retailer must verify a valid registry identification card and driver's license or other form of valid identification for all medical sales of cannabis. These sales must be accounted for and tracked separately from adult use cannabis sales.

No. However, both Cannabis Excise Taxes are imposed on bundled transactions that contains cannabis and cannabis products along with other items sold for one price.

No additional taxes exist simply for the delivery of cannabis.

Yes, all adult use cannabis sales delivered to the customers’ address are subject to the State and Local Cannabis Excise and Sales and Use Tax. The Local Cannabis Excise Tax should be reported under the city/town where the delivery took place.

Otherwise, the Local Cannabis Excise Tax for all sales made on premise, should be allocated to the city/town where the retail establishment is located.

Yes, a permit is required for each location.

Yes. The State and Local Cannabis Excise Taxes do meet the definition of Trust Fund Taxes as they are collected from the customer and held in trust for the State. In the case of the Local Cannabis Excise Tax, the tax is then distributed to the city or town where the product is delivered.

Generally, the statute of limitations for assessment is three (3) years from the date a return is filed. However, if the retailer fails to file a return, the Division may apply a six-year limitations period or other period supported by the statute.

This chart summarizes requirements for Adult Use Cannabis and Medical Cannabis with respect to taxes and forms that need to be filed/paid:

Filing Options

The Adult Use Cannabis Tax must be filed electronically using the RI Division of Taxation's Tax Portal

Resources

Advisory: 2022-36 Taxation of Adult Use Recreational Cannabis

Statutes:

Cannabis Tax - R.I. Gen. Laws § 44-70-1

The Rhode Island Cannabis Act - R.I. Gen. Law § 21-28.11

Regulations:

Division of Taxation Regulation: Link will be provided once the regulation is finalized

Office Of Cannabis Regulation: https://dbr.ri.gov/office-cannabis-regulation

Contact Us

Excise Tax Section

Email: Tax.Excise@tax.ri.gov

Telephone: 401.574.8955